Co-written with Simon Young, CEO of CaribRM

Despite its various detractors and setbacks, microcredit — the leading product in the ongoing microfinance revolution — remains an incredibly valuable tool in the international economic development tool chest.

This being said, microcredit has limited capacity to alleviate poverty on its own. To support widespread sustainable economic development, a host of attendant financial tools is required; hence the advent of and increased attention paid to “alternative” microfinance products such as microinsurance. Whereas microcredit provides low-income persons primarily with the ability to increase their earning potential or quality of life, microinsurance — when designed effectively and efficiently — gives them the ability to withstand and rebound from unpredictable, irregular and severe loss events and to sustain the process of individual economic development often initiated by a microloan.

The innovation imperative

The challenges that beset the process of microinsurance product development include the unique magnitude, diversity and nature of risks affecting the poor. Simply downscaling existing commercial products does not work. Instead, for insurance companies to access the low-income marketplace, entirely new business models are required so as to streamline delivery and administrative processes without compromising product and service effectivity.

Such an innovation imperative erects a significant barrier to entry, which explains why, despite the tremendous commercial promise of a $40 billion insurance market at the bottom of the global socio-economic pyramid, the microinsurance market remains largely underdeveloped, particularly for natural catastrophe risk. Such a marked lack of insurance among poor populations should be of keen interest to donor governments since, as the effective “insurers of last resort” and guardians of society’s moral imperative, losses affecting the uninsured inevitably fall on public budgets.

Catastrophes, climate change and social protection

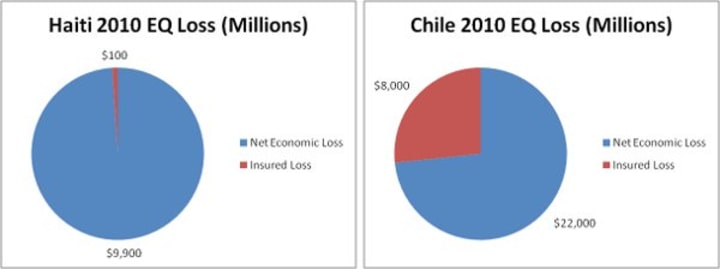

The dramatic socio-economic effects of this market shortfall are made most apparent after a catastrophe. Take, for example, two earthquakes that occurred in the Latin America and Caribbean region in 2010, one in Haiti and the other in Chile. While the economic loss from the Haiti earthquake was only a third the total size of the economic loss from the Chile earthquake, its size relative to gross domestic product was much higher (152 percent versus only 15 percent in Chile). To make matters worse, only 1 percent of the total loss in Haiti was insured versus nearly 30 percent in Chile.

Click here to see the image in large size.

The increased uptake of insurance in more developed markets works to expedite economic recovery — in Chile, the post-disaster economy has exhibited robust growth. Whereas in less developed markets, a lack of insurance penetration increases reliance upon often capricious donor aid and inhibits recovery, in Haiti, funds pledged were slow to arrive, inhibiting economic recovery.

The above comparison serves to underline the importance to donor countries and aid institutions of developing effective disaster risk management strategies which simultaneously protect public budgets and improve the resiliency of low-income populations. Supporting the development of ex-ante social protection mechanisms such as microinsurance will enable vulnerable populations to manage their risks proactively and recover from loss more readily. While this may seem something of a platitude, the urgency behind the effective development of such programs is only increasing in the face of a variety of 21st-century risk factors — most notably climate change.

Though the incidence of earthquakes remains unaffected by changes in the global climate, an increasing frequency of weather-related loss events has been noted worldwide. According to the 2011 Global Assessment Report on Disaster Risk Reduction, the global incidence of weather-related loss occurrences continues to rise alongside the risk of economic loss in all regions. Moreover, the severity of these more frequent events is magnified by a number of parallel growing trends, such as urbanization and coastal development, which increase societal exposures to weather-related losses. All of these unfortunate developments are clearly most threatening to the economies of low-income countries that have proportionately large vulnerable populations and limited methods of financial redress beyond foreign largesse.

Several initiatives are underway or in development to address the increased uncertainty and risk associated with climate change and its various contributing factors. Despite diverse charters and an array of desired outcomes, all focus to varying degrees on the development of a specific class of solution: index-based micro(re)insurance.

Innovations in index insurance

Index-based or parametric insurance products represent an extremely promising avenue for the implementation of effective and efficient catastrophe-risk-transfer mechanisms. These mechanisms will benefit the poor and are supportive of economic development, mainly due to their ability to streamline program administration and lower associated expenses. Since index insurance payouts are priced and trigger based upon an objective parameter, they do not require any of the detailed underwriting and loss adjustment processes used for traditional indemnity products. In nominal terms, this can reduce microinsurance expenses from more than 40 percent of total premiums for typical life and health programs to low single-digit percentages for index-based catastrophe programs.

However, as catastrophe events are often highly localized and the capacity of local markets to withstand risk varies, index-based products can prove rather difficult and expensive to design. The implementation and/or expansion of index-based microinsurance programs also remains hampered by a number of other external gating factors. These include data shortage, model development complexity, and a dearth of technical capacity, all of which lead to diminished or nonexistent financial capacity for risk transfer. Recognizing this reality, a litany of aid agencies and government-funded initiatives have begun to focus their efforts on promoting the significant research and development necessary to deploy effective, efficient and innovative index-based catastrophe covers, including the Microinsurance Innovation Facility, the Global Index Insurance Facility andthe Munich Climate Insurance Initiative.

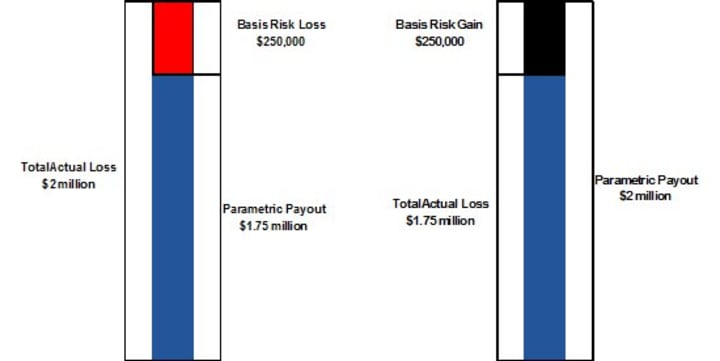

Despite the promise of index insurance and the high-profile initiatives mentioned above, few programs have attempted to address head-on what is arguably the most notable hindrance to the widespread adoption of parametric catastrophe microinsurance programs: basis risk. Basis risk — or the risk that an index-based contract payout will be greater (“basis risk gain”) or less (“basis risk loss”) than actual loss incurred by the index insured — is unavoidable to some degree in index insurance. However, it tends to be pronounced in a microinsurance context due to the general lack of detailed historical weather and exposure data in low-income markets. When index product payouts are insufficient to cover losses incurred by a low-income individual or community, the risk of irrecoverable reputational damage to the product is immense.

Click here to see the image in large size.

One initiative has endeavored to address the issue of basis risk directly. The Microinsurance Catastrophe Risk Organisation, or MiCRO, which was established by a consortium of strategic stakeholders earlier this year, has developed a hybrid parametric and indemnity risk-transfer platform which enables institutions serving the poor (notably multilateral financial institutions) to offer their clients catastrophe coverage linked to actual losses while obtaining bespoke and comprehensive institutional protection for their own account, thus effectively eliminating exposure to basis risk at the low-income client level and mitigating exposure to basis risk at the institutional level. The innovation enabling this solution is MiCRO’s unique basis risk transfer policy which allows (re)insured institutions to cover their exposure to basis risk losses arising from catastrophic perils covered inadequately on a parametric basis. MiCRO’s innovative coverage mechanism was adopted by Fonkoze, the largest MFI in Haiti, in 2011 and is presently being reviewed for adoption by a number of new clients worldwide.

The ultimate goal of the global risk transfer marketplace should be to provide low-income consumers and institutions serving the poor with the ability to transfer their catastrophe risk more readily and cost-effectively. More innovations are clearly required before indemnity coverage can be provided to low-income consumers directly without the probability of programmatic cost overruns. In this capacity, MiCRO represents an integral stepping stone on the path toward improved financial resilience for the poor and, in turn, their governments.

Tell us what you think! Comment below or tweet to @devex with #RioPlusSolutions, and catch up on other Rio+Solutions content here or on Facebook.

About the author

Alex Bernhardt

Alex Bernhardt is the founder and manager of Guy Carpenter's GC Micro Risk Solutions group. Under his direction, GC Micro now manages microreinsurance programs in Asia, Africa and Latin America. He also leads a multistakeholder project team that develops an index-based microreinsurance for small-holder farmers in Mozambique. He regularly contributes content to industry publications and speaks at international events.