WASHINGTON — Small agencies that work alone, siloed off from the rest of a country’s development work: That’s how development finance institutions might have been described just a decade ago. But DFIs have gained prominence as the role of the private sector has been accepted and because their work can be put in direct service of meeting the Sustainable Development Goals.

As the paradigm shifted from a focus on social service support and grant-based official development assistance to one more driven by private sector development, countries have turned to development finance institutions to provide solutions to help create jobs, spur economic development, and reduce poverty. As a result, the number of institutions has proliferated.

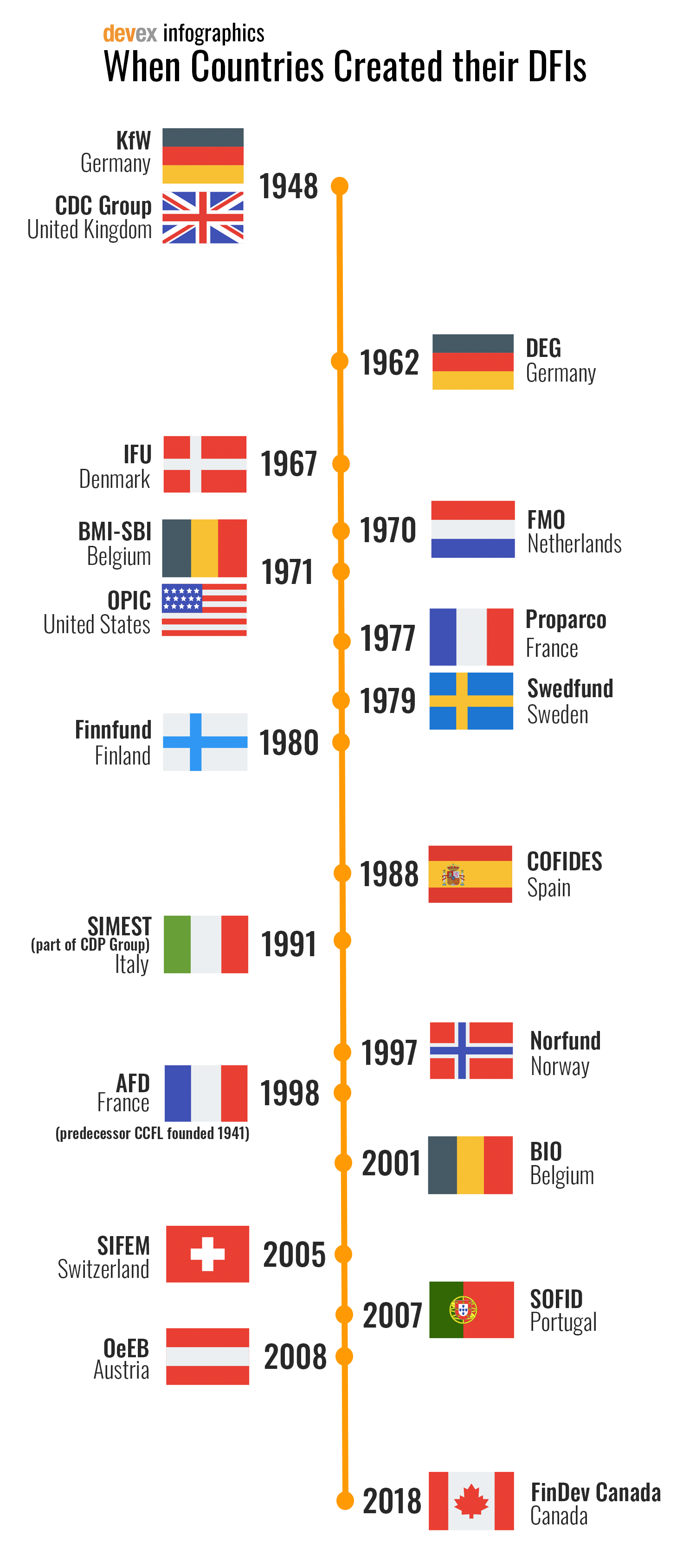

The United Kingdom has directed a big influx of capital toward its DFI, the CDC Group. Canada created a DFI in 2018, and the U.S. Congress will launch a new DFI this year with more capabilities and double the investment capacity than its current institution. Other countries, notably Australia, are considering creating DFIs.

For Devex Pro subscribers: What does the data tell us about DFIs?

Devex digs into the data behind DFIs to bring you emerging financing trends.

In 2017, bilateral DFIs were managing just over $65 billion in assets, according to data gathered by Devex, up from about $41 billion in 2012. That’s a roughly 57 percent increase in a five-year period.

Growth is clear in Europe, according to the Association of Bilateral European Development Finance Institutions, or EDFI. There were about seven active DFIs when the association for European DFIs was founded some 25 years ago; today there are 15. And the balance sheets of those DFIs tripled between 2005-2015.

“They did things that were relevant for development, but a number of them were financial institutions living a quiet life without any significant profile in any development policy of their countries,” said Soren Andreasen, the general manager at EDFI. “Many countries didn’t have economic development or private sector development policy as part of their aid strategy and none had [a] policy on how DFIs fit into private sector strategy.”

“One thing DFIs need to be more comfortable doing is rolling the dice for transformative impact.”

— Colin Buckley, chief operating officer, CDCAs DFI budgets grow and they play a more prominent role in development, they are also facing more scrutiny. DFI leaders are grappling with how to increasingly invest in least developed or low-income countries, how to ensure they are collaborating rather than competing, and how to effectively mobilize private capital rather than crowd it out. Amid calls for them to be more transparent, and to prove their investments are achieving development results, they are also working on new ways to measure their impact.

Taking risks

In the past several years, a number of DFIs moved to invest more in least developed or low-income countries.

Deals in LDCs are difficult and complex. They require taking more financial risk and more effort and creativity, said Colin Buckley, chief operating officer at CDC.

For Devex Pro subscribers: Profiling 17 development finance institutions

Devex delves into analysis and commentary of 17 bilateral development finance institutions.

Historically, DFIs have been hesitant to invest in fragile states and risky settings where the investment had less than an 80 percent probability of success, even if it had the capacity for transformative impact, Buckley said.

“One thing DFIs need to be more comfortable doing is rolling the dice for transformative impact,” he said.

DFIs will not, and cannot, solely invest in the poorest, riskiest places. In an effort to remain profitable and balance their portfolios, they will continue to make some investments that are deemed safer, even as they look to invest more in low-income countries.

But some experts believe that DFIs should be taking more risk and doing more to crowd capital into higher risk markets where private finance is especially scarce.

“Some DFIs — I’d pick on IFC [the International Finance Corp.] for sure here — are mostly not in high-risk markets and not very engaged in high-risk sectors and are mostly doing safe projects,” said Todd Moss, the executive director at the Energy for Growth Hub, a spin-off from the Center for Global Development, where he is also a visiting fellow.

Part of the problem has to do with incentives: At some DFIs, investment teams are rewarded based on the amount of money invested, rather than on where it is invested or what its impact will be. There is also often pressure on the financial side, especially for DFIs that operate like commercial banks and are trying to maintain AA or AAA credit ratings.

“The scale and risk issues mean for these agencies to succeed, they need to create internal incentives for people to take risk and subsidize upfront costs,” Moss said.

As DFIs look to take on more risk in pursuit of development impacts, they may also need to reevaluate their targets for financial rate of return and credit rating expectations — which in most cases, haven’t changed, even as DFIs look to work in riskier and potentially more impactful geographies and sectors, said Alix Zwane, CEO at the Global Innovation Fund.

“We may need new financing vehicles, special purpose vehicles off balance sheets, where risk is contained,” she said.

DFIs must also change their approach to how they create projects; otherwise they may find it difficult to deploy their capital, said San Bilal, head of the economic transformation and trade program at the think tank ECDPM. That is because in low-income countries, there are simply not enough projects that meet their investment criteria.

“There is no such thing as a passive investor in fragile state,” Buckley said, adding that CDC has found that it really needs to work alongside the businesses it invests in and hire additional staff to do so.

The European Fund for Sustainable Development, which was launched last year, is looking to provide technical assistance and has project preparation units to make more projects bankable. Bilal said more DFIs should consider providing this kind of technical assistance for better preparation or to support small- and medium-sized enterprises.

Without more vehicles working to make projects bankable, one of the dangers is that all DFIs are looking at the same potential projects, sparking concerns that limited public finance may crowd out the private sector and not ultimately improve the conditions, he said.

Competition

The challenge of competition — both among DFIs as they look to deploy their capital in markets with limited options, and with private actors — could have a negative effect on most of their missions to improve development and reduce poverty. Rather than competition, more cooperation is needed in the sector, several experts told Devex.

While DFIs might be hesitant to talk about it, one investor in Africa told Devex that in some sectors, he’s seen DFIs come in and undercut commercial investors in ways that can distort markets.

The investor said he believes that part of the cause is competition among DFIs for deals. This pushes loan pricing down and forces intermediaries to raise blended capital funds and get highly concessional financing from governments and donors in order to be able to attract some commercial capital at rates that they will accept.

As a result, in some industries, DFIs appear to be preventing a natural progression to more commercial capital over time, keeping them locked in as sectors dependent on concessional financing, he said.

Not all DFIs are investing in that way, the investor noted. He pointed to a recent Overseas Private Investment Corp. deal where OPIC made part of its investment junior debt, a move that would allow the fund to raise more commercial sources of capital, which would need to be senior debt.

“I dont think they’re chasing out private capital very often. The bigger problem is sometimes crowding in other DFIs rather than truly private capital,” Moss said, adding that it could be an issue of immature markets that would change over time.

Some, including Andreasen, said that they don’t see competition as a problem, and instead often see DFIs working together. About one-third of individual investments that the European bilateral DFIs make are done alongside other European DFIs, he said.

“It’s fine to have debate and scrutiny in this respect, but I don’t see a lot of specific evidence,” Andreasen said.

One place DFIs are playing a critical role, and are working together, is in financing local banks in Africa in the wake of restrictive regulations around risk that have led many commercial banks to pull out, he said.

Buckley said DFIs haven’t been very good at coordination with one another or with aid agencies. Often, transformative investments need regulatory or institutional reform — and that is where DFIs should work more closely with aid agencies to address some of those challenges.

“I think people should demand more cooperation as DFIs grow in prominence and capital,” Buckley said.

Transparency and measurement

As more funds are funneled through DFI investment mechanisms, demand is growing for better measurement and improved transparency.

“As public agencies, they should be as transparent as possible — they don’t need to release every detail of every project, but they should release information about activities ... as maximally as possible,” Moss said.

A DFI should release all information unless there is a commercial reason not to, he said. It should be transparent about systems for evaluating development impact during and after it makes investments, and the data should be made available in easily accessible formats.

“DFIs need to be better at looking at outcomes and impact and incorporating that kind of consideration in decision-making,” said Samantha Attridge, a senior research fellow at the Overseas Development Institute.

DFIs already collect a lot of data on operations and direct project effects, for example, on job creation and tax creation and growth. But one of the challenges is the need to better understand indirect effects on the supply chain and the broader economy, Attridge said.

For example, a project should not just measure direct jobs but evaluate if the investment displaced jobs and look at the quality of the jobs. A power project should look at the affordability of power when trying to determine benefits of access, she said. And as those impacts are counted, DFIs need to figure out how to ensure that the benefits aren’t double counted in deals with multiple investors, she said.

DFIs are investing a lot of time into establishing frameworks to understand what development impact is, and how to track transactions and their impact, Andreasen said.

That measurement isn’t easy, but there are models that DFIs can use, GIF’s Zwane said. One option is to model the net present value of social returns for a social return on investment calculation akin to a calculation for a financial return, she said.

The role of development finance institutions is evolving. Through a series featuring interactive data visualizations and interviews with DFI leaders, Devex is exploring their growing influence, where they are investing, and key challenges they face. Explore the series.

For more innovative, early-stage projects, there may not be enough information to determine a credible social return on investment metric from the start, which is a challenge that funds such as GIF have faced. When it can’t calculate a social return on investment at the beginning, it tries to share information about how many people will be impacted, the depth of impact, and what the probability is of success, she said.

That work requires both money and staff time, and while there may be a growing interest in measuring impact, some DFIs haven’t fully grappled with the implications for funding and staffing an impact measurement structure, Zwane said.

CDC has been working on a new development framework and has a DFID-funded evaluation facility with an independent board that has allowed it to do more evaluations, test the development impact thesis of its projects, and help businesses adapt, Buckley said. In the evaluations CDC is looking at everything, from lean data to 10-year longitudinal evaluations, he said.

“The reason that’s important, the reason that you need to have that development impact clarity is that when we are clear about why we are making an investment, what development impact we expect it to have, that allows us to navigate the troubled waters you inevitably run into in troubled geographies,” he said.

More cooperation on this issue in particular could lead to better standardization or industry standards that could allow more DFIs to accept more risk in exchange for higher social return, Zwane said. And that data — the numbers and the narrative — will help DFIs define and communicate their evolving role in the development landscape.

Vince Chadwick contributed reporting to this article.

Update, April 16, 2019: The timeline graphic in this article has been updated to correct the date that Proparco was founded.

About the author

Adva Saldinger@AdvaSal

Adva Saldinger is a Senior Reporter at Devex where she covers development finance, as well as U.S. foreign aid policy. Adva explores the role the private sector and private capital play in development and authors the weekly Devex Invested newsletter bringing the latest news on the role of business and finance in addressing global challenges. A journalist with more than 10 years of experience, she has worked at several newspapers in the U.S. and lived in both Ghana and South Africa.

Search for articles

{kind=link}

Most Read

- 1

- 2

- 3

- 4

- 5