Despite increased attention on the need to bridge the global financial inclusion gap, much of the adult population in the developing world still does not have bank accounts. Many do not have convenient access to traditional financial services either. But the gap is decreasing, a recently released report on financial inclusion finds.

Co-authored by teams from the International Finance Corp. and the Consultative Group to Assist the Poor, “Financial Access 2012: Getting to a More Comprehensive Picture” analyzes — for the first time — not only “supply-side” data from IMF’s Financial Access Survey, but also global “demand-side” information from the World Bank’s Global Findex database. While FAS has been gathering and publishing data since 2009, Global Findex only released the results of its survey last year.

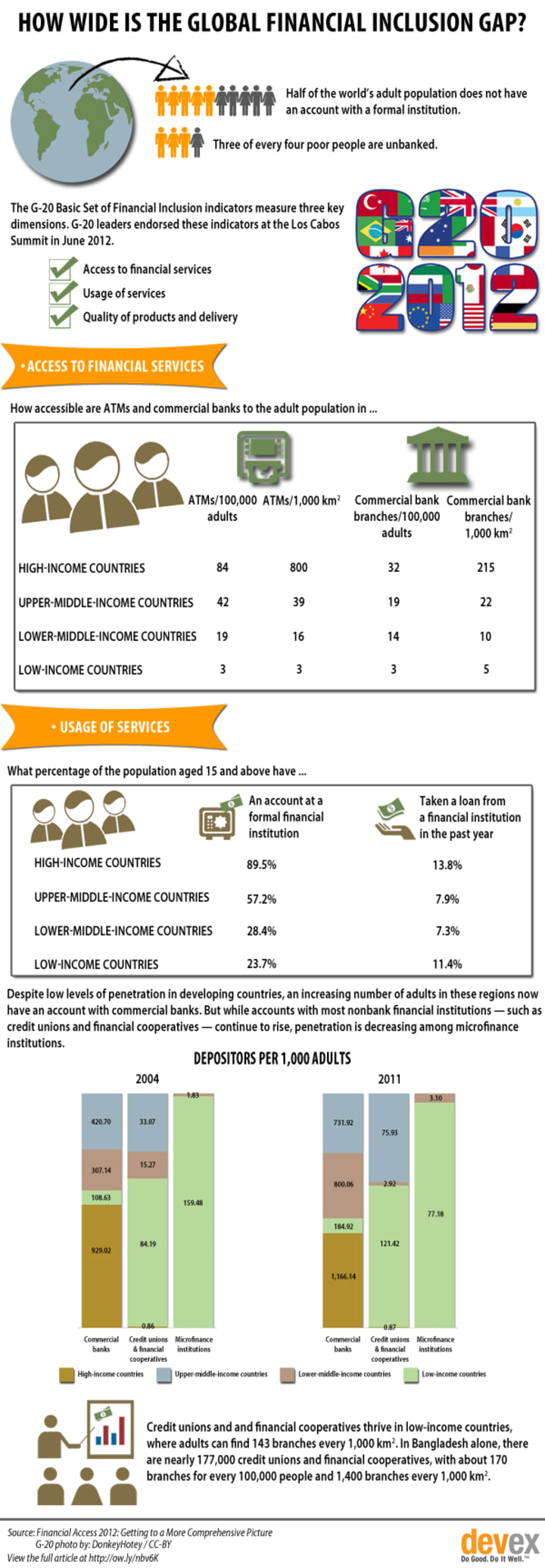

Lower-middle-income countries posted the highest increase in the number of depositors at commercial banks. For every 1,000 adults in the region, more than 800 had bank accounts in 2011, up 26.1 percent from 2010. But the number of depositors at credit unions and financial cooperatives plummeted 88.7 percent to just nearly 3 for every 1,000 adults in lower-middle-income countries.

Credit unions and financial cooperatives are more deeply entrenched in low-income countries, where there are at least 7,700 such institutions regionwide — the majority of which are in sub-Saharan Africa. But as more of these pro-poor entities transform into commercial banks, the number of adults with bank accounts in 2011 increased 5.3 percent to almost 185 for every 1,000 legal age residents in low-income countries.

Commercial banks are also gaining ground in low and lower-middle-income countries because of the partnerships they are making with semi- and informal financial institutions. An increasing number of banks are now engaged in providing mobile money services and refinancing to microfinancing institutions. In addition, a lot of these microfinancing institutions are now licensed to operate as banks, which explains to some extent the 25.8 percent drop among depositors and customers in low-income countries.

But despite notable advancements in commercial bank penetration, nonbank financial institutions — which include not only credit unions and financial cooperatives, and microfinancing institutions, but also rural and agricultural banks, building societies, and savings and loan institutions — continue to dominate the financial landscape in low-income countries.

Click on the image to view a larger version of the infographic.

Read more:

Join the Devex community and gain access to more in-depth analysis, breaking news and business advice — and a host of other services — on international development, humanitarian aid and global health.

About the author

Aimee Rae Ocampo

As former Devex editor for business insight, Aimee created and managed multimedia content and cutting-edge analysis for executives in international development.