Just 10 years ago, in many places across the world it was common for shopkeepers to have to close their businesses while they traveled to a bank to make a deposit, for families to wait in long queues to pay school fees, and for workers to send envelopes of cash home to their families by taxi or bus.

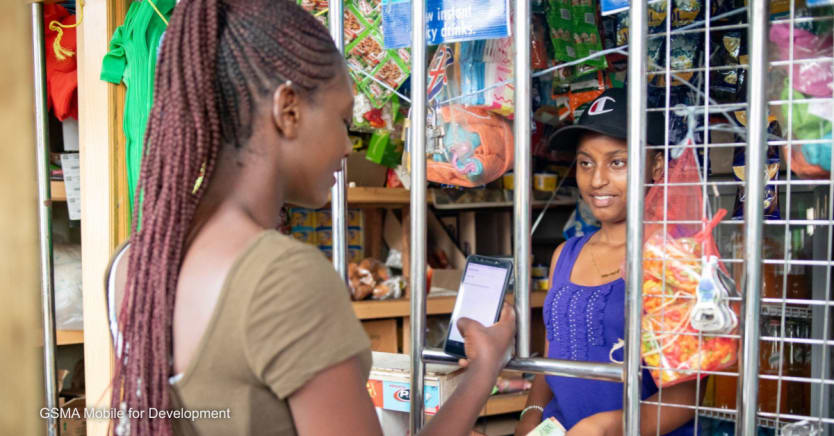

For tens of millions of households, this all changed as mobile money expanded from a niche offering in a handful of markets to become a mainstream financial service. Armed with just a mobile phone and a mobile money account, deposits, payments, and remittances became convenient and secure. Urban residents could access and pay for basic utilities, smallholder farmers could get paid directly for their crops and build a credit history, and populations caught up in humanitarian crises could receive rapid financial relief.

This year, the GSMA Mobile Money program is celebrating 10 years of the “State of the Industry Report on Mobile Money.” To celebrate, the team hosted a live launch moderated by GSMA Director General Mats Granryd, with high-profile speakers from the United Nations, the World Bank, the Bill & Melinda Gates Foundation, and M-PESA Africa.

Catch up on the session here to dive into the profound impact of mobile money on financial inclusion and the huge opportunities still to be explored.

Still, this pathway to the formal economy has not been opened to everyone. Hundreds of millions of people remain outside the formal financial system with no safe, easy, or reliable way to receive money, pay bills, take out a loan, buy insurance, or store their savings.

Across low- and middle-income countries, women are less likely than men to have a mobile money account. Even when people have a mobile money account, they run up against barriers to using it. Around 1 billion registered mobile money accounts are not active on a monthly basis, for reasons ranging from low literacy and digital skills, to unreliable mobile networks, or feeling that mobile money is not relevant to their lives.

There is no easy path to financial inclusion, but mobile money has proven to be one of the most accessible and practical ways to breakdown traditional barriers to the financial system and unlock access to life-enhancing services. Even more profound benefits are possible — if we can overcome the barriers.

A decade of progress and change

Thanks in part to mobile money, people are living increasingly digital lives. According to the GSMA’s 10th annual “State of the Industry Report on Mobile Money,” there are 1.35 billion registered mobile money accounts, 10 times more than there were in 2012. In 2021, the annual value of mobile money transactions hit a record $1 trillion. This is nearly $2 million transacted each minute.

The everyday impacts of mobile money have been transformative, and the past decade has shown the power of mobile money to strengthen financial resilience.

For example, the GSMA’s 2021 Global Adoption Survey found that 44% of mobile money providers offer credit, savings, or insurance products. For informal workers, micro-, small-, and medium-sized enterprises, and low-income communities with irregular incomes, these products can provide a financial lifeline in times of crisis and an important safety net, allowing them to invest in their livelihoods, build their credit profile, and improve their standard of living.

The COVID-19 pandemic has made mobile money even more vital. Reluctance to handle cash caused merchant payments to skyrocket, and more companies shifted to paying salaries directly into their employees’ accounts, while governments worked with mobile money providers to deliver much-needed pandemic relief payments.

Mobile money-enabled sustainable development

Over the past decade, humanitarian organizations have rapidly increased the amount of cash and voucher assistance, or CVA, they provide to individuals affected by crises. Compared with in-kind aid, CVA can be delivered more quickly, provide greater choice and dignity, and support local markets.

Recently, the sector has been transitioning to digital payment systems, such as mobile money and ATM cards, instead of cash in envelopes where possible. Not only has this made humanitarian assistance more efficient and transparent, but it has also provided a safer and more accessible option that also opens the door to financial inclusion.

One in 3 urban residents still lack access to water, sanitation, and energy, but mobile money is helping to close the divide. Mobile money-enabled payments, combined with smart meters and other innovations, are improving the customers’ experience and agency, while enhancing revenue collection and data-driven decision making for utility providers.

In off-grid areas, pay-as-you-go solar home systems are supplying millions with clean and affordable power for the first time, allowing shopkeepers to stay open longer, children to do their homework in the evenings, or health clinics to serve more patients.

Smallholder farmers are the backbone of rural economies and a major part of global food production, but only about one-third of their financing needs are being met. Agricultural digital financial services are bringing smallholder farmers into the digital economy with digitized payments, allowing crop buyers and others in the value chain to pay farmers directly into their mobile money accounts.

Mobile gender gap increased during pandemic, new data shows

Women are now 16% less likely than men to use mobile internet, up from 15% last year, after that figure had steadily declined each year from 25% since 2017.

This has provided a much-needed entry point to savings and credit products, as data generated in part from their mobile money transactions is used to create economic identities that banks and other lending institutions can use to assess farmers’ creditworthiness and issue loans.

The next 10 years

Mobile money is empowering people to access savings and investment opportunities, recover from financial shocks and crises, and build resilience to climate change. Yet, even more profound benefits are possible if we can close the mobile gender gap, activate the more than one billion registered mobile money accounts that are not active monthly, and meet their diverse needs.

This could mean delivering faster and more secure cash transfers to the at least 274 million people in need of humanitarian assistance; providing credit, insurance, and other risk management tools to some 500 million smallholder farmers growing one-third of the world’s food; and unlocking access to affordable, reliable and safe water, energy, and sanitation for the more than 1.2 billion people without access to core urban services.

About the author

Max Cuvellier

Max Cuvellier leads the Mobile for Development team at the GSM Association, partnering with bilateral donors, private foundations, mobile operators, entrepreneurs, investors, governments, and international NGOs in Africa, the Asia-Pacific region, and elsewhere to improve access to basic services for local populations through technology.