The World Bank and International Monetary Fund annual meetings kick off Monday in Washington amid a unique confluence of crises — not least the fallout from the pandemic, the war in Ukraine, inflation, a weakened Chinese economy, and climate change.

Unless you vividly remember the disco era of the 1970s, you’ve never lived through a set of economic circumstances remotely like the current moment. Inflation is rampant, inequality is rising, and poverty rates have stopped declining. Hunger is threatening to spread more widely and, historically, social unrest often follows.

Between the annual meetings, the 27th United Nations Climate Change Conference, or COP 27, shortly afterward, and the G-20 leaders’ meeting in Indonesia in November, there is a sense that there’s only a small window to get the remedies right and facilitate a soft landing to the turbulent ride.

For the world’s low-income countries, there is a real chance that getting it wrong will lead to a “lost decade” for their economies.

This all makes for a busy agenda at the meetings, which are back to being fully in person after two years of being held virtually or in hybrid format. In an era where policymakers are openly admitting there are no great options, and after many got it wrong on inflation and other key issues, are multilateral institutions capable of stepping up?

In a blunt interview with Devex, Indermit Gill, the new chief economist of the World Bank, said that workers and families around the world are facing tough times ahead.

“Things are likely to be worse for you, unless governments do a really good job of walking this very tight path between cutting inflation and keeping growth going,” he said.

Central banks are raising interest rates to cool an overheated economy, but they could trigger a recession, especially with all major central banks tightening at the same time. Gill said policymakers were too slow to hike rates last year, and now may be too quick and aggressive as they catch up.

IMF Managing Director Kristalina Georgieva was similarly gloomy Thursday as she addressed students at Georgetown University, where she stated that even if we don’t meet the technical definitions for a recession, “it will feel like a recession because of shrinking real incomes and rising prices.”

At a press conference Friday, Gayle Smith, the head of the ONE Campaign, argued the sheer number of problems has created “the most acute crisis we’ve ever witnessed.” She said policymakers have just a small amount of time to create a “global economy that actually functions.”

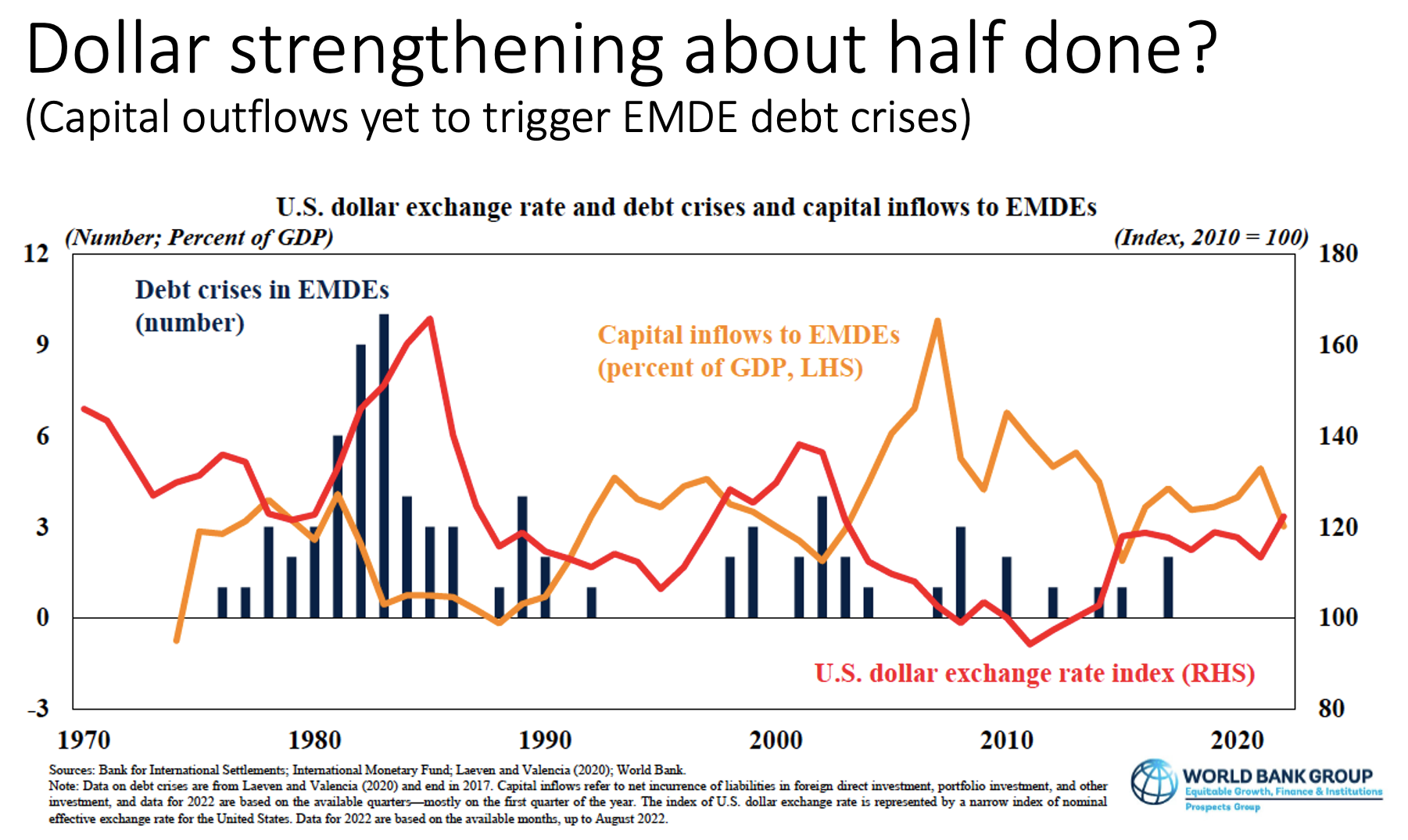

The current economic cycle has particularly bad news for low- and middle-income nations. Capital outflows from emerging markets are picking up pace — contributing to a strong U.S. dollar and adding to inflation problems for countries that import food and energy.

Moreover, many low-income countries are in debt distress or facing the prospect of hitting this dire state, and if they have bonds denominated in the U.S. dollar, repaying them is becoming harder.

This means that more and more countries are using limited resources to service debt, rather than being able to put that cash to use for health service, infrastructure development, and projects that will create jobs and increase their citizens’ well-being.

In sub-Saharan Africa, for example, the World Bank warns that debt levels are setting off alarm bells. Governments were spending 16.5% of their revenues servicing external debt in 2021, up from less than 5% in 2010.

“Things are likely to be worse for you, unless governments do a really good job of walking this very tight path between cutting inflation and keeping growth going.”

— Indermit Gill, chief economist, World BankIt’s only getting worse. And as officials at both the bank and the IMF say, countries often refrain from asking for help until it is too late, fearing the stigma of admitting they have a problem.

The other issue, as we have reported repeatedly, is that debt is no longer owed primarily to a group of wealthy Western creditor nations and the Bretton Woods. And China, which has become a key lender to lower-income countries, is seen as dragging its feet on restructuring deals.

Part of the challenge, especially for the IMF, is to find ways for governments to seek assistance without getting punished by investors on capital markets. Moreover, if countries are too deeply indebted, they may not be able to get an IMF program in the short-term, presenting another roadblock to preventing more chaos.

At the global level, one of the strongest indicators of the “crisis in development,” to borrow a phrase from World Bank President David Malpass, is the near-total stagnation in poverty reduction.

The bank recently said the world will not meet the United Nations Sustainable Development Goal of eradicating extreme poverty by 2030, with 600 million people still expected to be in the most dire straits in that year.

While COVID-19 significantly contributed to the setbacks, another issue is the war in Ukraine, which has caused food and fertilizer prices to spike, hurting the most vulnerable and pushing people into poverty, which is being compounded by the strong U.S. dollar.

One of the big questions hanging over the annual meetings is reform of the multilateral development banks. Earlier this year, a group of experts produced a report for the G-20 arguing the banks can lend hundreds of billions more, by taking on more risk and using innovative financing.

The report has faced pushback from credit rating analysts, who have warned the World Bank and others risk losing their coveted AAA ratings if they stretch their balance sheets further.

Speaking ahead of the annual meetings, U.S. Treasury Secretary Janet Yellen on Thursday called for the banks to “evolve,” and said she wants a specific roadmap for the World Bank by December. She also, surprisingly, mulled letting middle-income countries borrow from anti-poverty lenders at concessional rates for climate mitigation.

“No country can tackle it alone,” Yellen said of climate change, as she called for reforming the multilateral development banks to tackle more global challenges. Historically, they have been country-focused, and such a change would be a seismic shift.

Of course, Malpass himself has been in the crosshairs over his “I’m not a scientist” climate bungle last month. Despite backtracking repeatedly and setting out on a campaign to highlight the bank’s increased lending for climate mitigation and adaptation, he is still in the hot seat.

Meanwhile, many of the bank’s biggest shareholders are backsliding on climate targets as they seek to meet their own energy needs. Europe, in particular, is facing a crisis because of the war in Ukraine. Devex has reported on the charges of “hypocrisy” being leveled at the wealthiest nations.

A recent report by Friends of the Earth noted that the United States, through its Export-Import Bank and the International Development Finance Corporation, provided $51.6 billion for oil and gas projects from 2010 to 2021. That’s five times the amount it spent on renewables.

At an event Thursday, Masood Ahmed, the head of the Center for Global Development, warned about perceptions that the wealthy nations treat natural gas as a “clean fuel for us, but a fossil fuel for the rest of the world.” He called this a “perceived double standard on energy” that must be addressed.

Other experts concur and add that getting the poorest countries on board with an aggressive climate agenda will require fairness. This means historic polluters will need to put their money where their mouth is and meet promises on climate finance — notably the pledge of $100 billion in annual funding that has never been met — to ensure the energy transition both happens and does not hurt the most vulnerable.

As Gill, the World Bank’s chief economist, said, without providing climate finance on fair terms to the low-income countries that have barely contributed to climate change, in a way that ensures they can develop and kill off indigence, then “implicitly what you're saying is that future generations in those countries are actually going to be poor.”

And that, he said, is not acceptable.

Printing articles to share with others is a breach of our terms and conditions and copyright policy. Please use the sharing options on the left side of the article. Devex Pro members may share up to 10 articles per month using the Pro share tool ( ).

About the author

Shabtai Gold

Shabtai Gold is a Senior Reporter based in Washington. He covers multilateral development banks, with a focus on the World Bank, along with trends in development finance. Prior to Devex, he worked for the German Press Agency, dpa, for more than a decade, with stints in Africa, Europe, and the Middle East, before relocating to Washington to cover politics and business.

{kind=link}