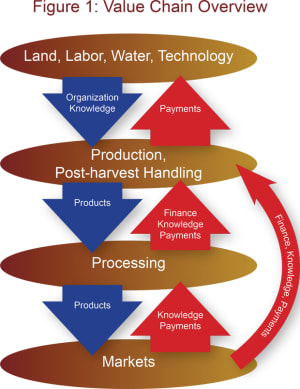

A value chain is a set of linked activities that work to add value to a product; it consists of actors and actions that improve a product while linking commodity producers to processors and markets.

Value chains work best when their actors cooperate to produce higher-quality products and generate more income for all participants along the chain, as opposed to the simplest kinds of value chains, in which producers and buyers exchange only price information — often in an adversarial mode. Value chains differ from supply chains, which refer to logistics: the transport, storage and procedural steps for getting a product from its production site to the consumer.

See more #FeedingDev articles:

• Want to include smallholder farmers in development models? Align interests

• It's high time India stands up for its malnourished children

• Food security and nutrition — 2 sides of the same coin

• 4 ways climate change causes world hunger

A value chain encompasses the flow of products, knowledge and information, finance, payments, and the social capital needed to organize producers and communities.

Information is especially important to all value chain actors and flows in two directions: markets inform producers of price, quantity and quality needs, product handling and technology options, while producers inform processors and markets on production quantities, locations, timing and production issues. In a value chain, processors and marketing agents may provide producers with finance, inputs and training in technologies of production.

Value chains may include a wide range of activities, and an agricultural value chain might include: development and dissemination of plant and animal genetic material, input supply, farmer organization, farm production, post-harvest handling, processing, provision of technologies of production and handling, grading criteria and facilities, cooling and packing technologies, post-harvest local processing, industrial processing, storage, transport, finance, and feedback from markets.

Agriculture in developing countries often is characterized by dual value chains operating in parallel for the same product: one informal or traditional, and the other formal or modern. Small holders are frequently involved in informal chains that deliver products to local middlemen and then to small local stores. Formal value chains can deliver the same product, usually in better or more uniform quality, from larger farms or more organized groups of small farmers to more commercial wholesalers and from there to supermarkets or exporters. This duality has been accentuated by the explosive growth of supermarkets in developing countries. It can limit many small producers to markets characterized by low-quality products, and low prices and low returns for them — hence a frequent concern is to find ways to integrate small producers into more modern value chains, both domestic and export-oriented.

Value chain analysis

A value chain approach in agricultural development helps identify weak points in the chain and actions to add more value.

In Rwanda, for example, analysis of the dairy value chain identified critical needs for more local milk cooling points, more collaboration between dairy plants and farmers and greater diversification of final products. In Guatemala, the world’s largest producer of cardamom, reviews by Heifer International and the Norman Borlaug Institute for International Agriculture revealed that critical value chain weaknesses are total lack of varietal development over 100 years and lack of development of more diversified markets for cardamom as an input to processed foods, cosmetics and health products. In the Philippines, the analysis found a need for fishermen to deliver more uniform-sized fish to processors, for government to enforce corresponding regulations and for processors to offer fishermen contracts that contain credit. And in Vietnam, a value chain analysis of a cassava industry driven by growing demand inside the country and from China identified issues regarding depletion of soil fertility (unsustainable farming methods), management of wastewater from starch plants, and the need for better direct links between small farmers and processors.

Another example is sorghum in Africa. It has multiple end uses, including as porridge, flour, snacks, couscous and other products for human consumption; inputs for beer production; and feed for poultry and animals. However, yields of these grains have increased only slightly, and the sales of the grains to markets other than animal feed face obstacles in the value chains. Farmers could expand their profits from these multiple potential markets if solutions were found for value chain issues such as:

1. Poor quality of seeds and varieties inappropriate for the various uses.

2. Poor quality of product at harvest, with grains of inconsistent size and coloration.

3. Inadequate threshing techniques and post-harvest drying and storage, which reduce quantity and market quality.

4. Inadequate grading.

5. Insufficient market development and communication with markets regarding varieties and quality of sorghum desired.

6. Insufficient training and finance for improved post-harvest management.

This analysis underscores the importance of sorghum growers and breeders recognizing that managing for food quality can increase their access to more markets. In Uganda, a brewery strengthened the sorghum value chain by offering farmers production contracts with guaranteed prices along with quality requirements, which led many more farmers to grow the grain.

Join the conversation at our LinkedIn group!

As these examples illustrate, finding ways to improve value chains can be very important for raising small holders’ incomes. Without being linked into markets they are condemned to produce only for subsistence — better markets can lift them out of poverty. But making this leap requires more knowledge, and many actors along the value chain can help supply this crucial ingredient.

Want to learn more? Check out Feeding Development's campaign site and tweet us using #FeedingDev.

Feeding Development is an online conversation hosted by Devex in partnership with ACDI/VOCA, Chemonics, Fintrac, GAIN, Nestlé and Tetra Tech to reimagine solutions for a food-secure future from seed and soil to a healthy meal.

About the author

Roger Norton

Roger Norton is regional director for Latin America and the Caribbean at the Norman Borlaug Institute for International Agriculture. He is a research professor of agricultural economics at Texas A&M University and has served as policy advisor and project team leader with experience in 48 countries. He was a director of research at the World Bank and has led research teams and training courses in developing countries across the globe.

Search for articles

.png?1406558424){kind=link}

Most Read

- 1

- 2

- 3

- 4

- 5